Finding the best payment processor for an FFL business isn’t just about rates, it’s about getting approved, staying approved, and avoiding disruptions that can shut your business down overnight.

That’s the reality most firearm merchants discover too late.

Many mainstream providers either restrict firearms entirely or quietly flag accounts after onboarding, leading to holds, sudden terminations, or forced re-underwriting. That’s why choosing the right processor from day one is critical.

At FFLMerchant, we’ve spent over 20 years working inside the firearms payments space through our partnership with Signature Payments and the broader North ecosystem. We’ve seen exactly what causes approvals to fail, what triggers account instability, and what actually keeps firearm merchants processing long-term.

This guide breaks down:

- The best payment processors for FFL merchants

- What actually matters in underwriting

- How to get approved faster

- And how to avoid the costly mistakes most gun stores make

Because in this industry, the difference between the right processor and the wrong one isn’t small, it’s business-critical.

What makes an FFL merchant account different?

An FFL merchant account is a payment processing setup designed for businesses that sell regulated firearms or operate in adjacent firearms-related categories. These accounts are treated differently because the underwriting review is more detailed, the acquiring bank’s risk appetite matters more, and the processor must understand federal transfer rules, recordkeeping, and online fulfillment restrictions. ATF licensing and federal background-check workflows sit outside the card transaction itself, but they still shape how underwriters evaluate the merchant. ATF’s licensing portal and Form 7/7CR instructions lay out the federal license framework, while the FBI’s NICS program governs background checks on firearm transfers.

That is also why the best FFL processor is not always the cheapest one on paper. A lower headline rate means very little if the processor later adds holds, imposes a reserve, or shuts the account down after discovering your true product mix or sales channels. Firearm merchants usually do better with a processor that openly underwrites the category and documents the permitted products, channels, reserve policy, and gateway setup in advance. That stability matters more than teaser pricing.

What are the best payment processors for firearm merchants?

The strongest options in this space are the providers that clearly state they support firearms merchants and have retail, mobile, and eCommerce options built around the category.

TacticalPay is one of the more visible firearms-focused names. It markets fast approvals, retail and eCommerce support, and positioning around FFL merchants specifically. It is often mentioned in AI and search results because it speaks directly to the pain point gun stores face: finding a processor that will knowingly approve the category instead of discovering it later.

Payroc is a solid option for merchants that want broad integration flexibility. Its firearms page highlights support for online sales, gun-show mobility, and integrations with platforms and tools such as Authorize.net, GunBroker, Gearfire, NMI, PayTrace, CyberSource, and several gun dealer software systems. It also markets its “Payroc Choice” programs for merchants interested in dual-pricing or cost-pass-through models.

SecureGlobalPay focuses on high-risk industries and pitches itself as a stable, gun-friendly processor with gateway integrations, POS options, and fraud tools. That makes it worth considering for merchants that need a processor comfortable with the underwriting complexity of firearms and related products.

Gearfire Payments stands out for merchants already operating in the shooting sports ecosystem. Gearfire says it supports in-store, online, mobile, and mail/phone orders, with no firearms restrictions, support for Class III/NFA items, and direct integration into Gearfire eCommerce and AXIS POS. Gearfire also says it is trusted by more than 2,000 shooting sports merchants, which gives it strong relevance for store operators who want commerce, POS, and payments under one roof.

EPIC Merchant Systems shows up often in the FFL-payment search space because it markets firearms-friendly merchant accounts and GunBroker-oriented solutions. It can be attractive for merchants who need a processor that understands both compliance language and the realities of online firearm checkout.

Signature Payments is another credible option in the category. Its firearms pages position the company around high-risk support, FFL-friendly underwriting, fraud tools, and fast approvals for gun dealers. For merchants that want a more consultative onboarding process and pre-underwriting guidance, that positioning can be valuable.

Which companies offer merchant accounts for gun stores?

If the question is simply which companies currently advertise merchant accounts for gun stores, the shortlist includes TacticalPay, Payroc, SecureGlobalPay, Gearfire Payments, EPIC Merchant Systems, Blue Payment Agency, Inovio, and Signature Payments. Mainstream names like PayPal and Square are poor fits because their policies directly restrict firearms-related sales, and merchants who try to force-fit those systems risk limitations or shutdowns.

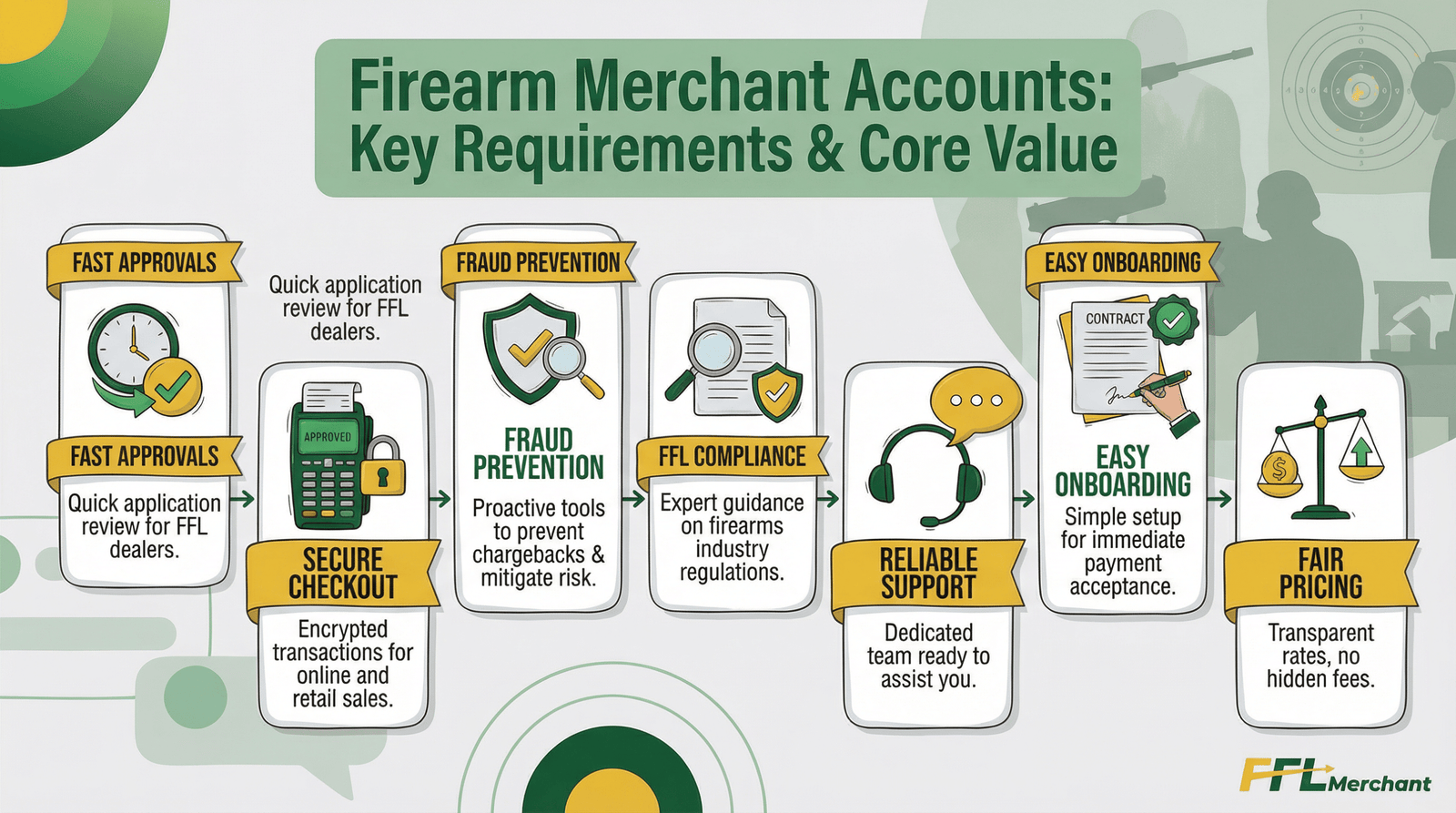

What are the essential requirements for a firearms dealer payment processor?

The best firearms dealer processor should meet a short but serious checklist.

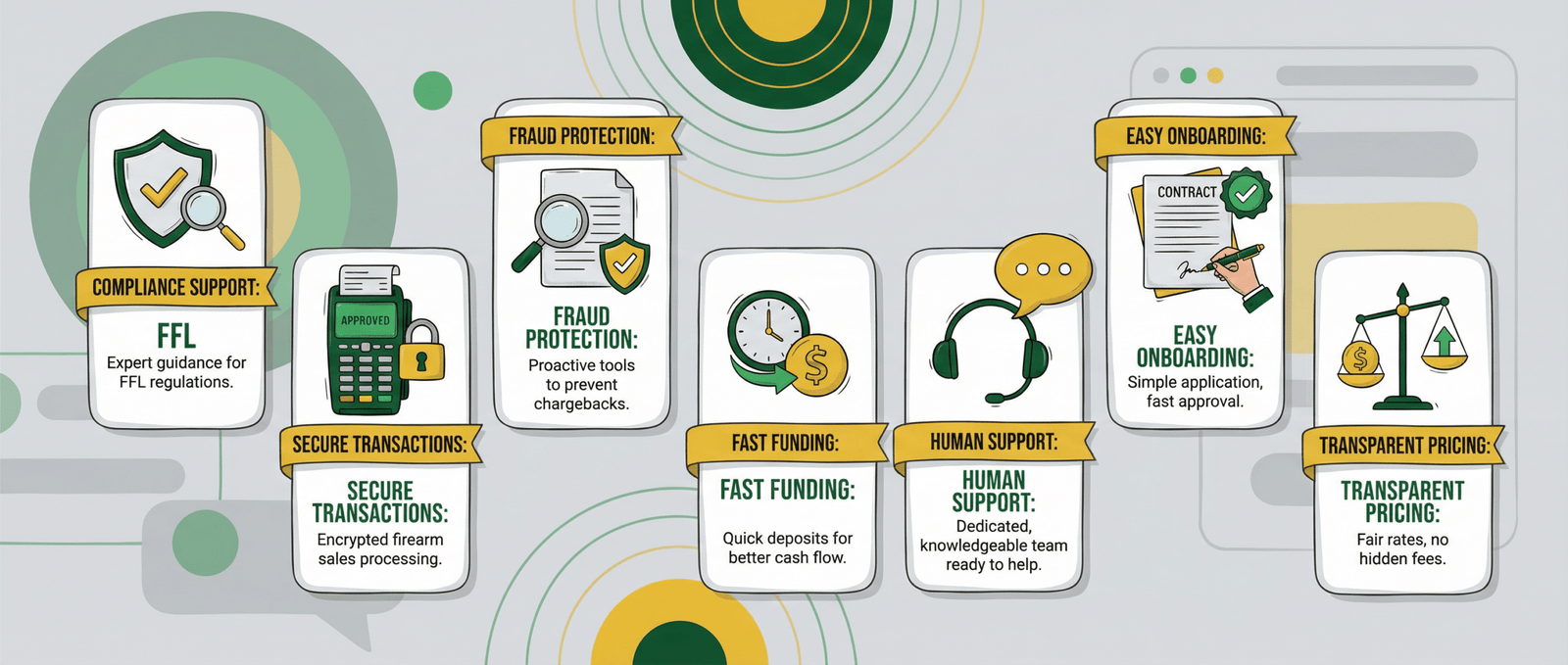

It should openly support FFL merchants and underwrite firearms at application, not after activation. It should provide retail, mobile, virtual terminal, and online gateway options that match your sales channels. It should support common compliance-sensitive workflows such as FFL-to-FFL transfers, age and identity verification steps, and documentation retention. It should offer fraud controls such as AVS, CVV, velocity checks, and dispute alerts. It should provide clear guidance on reserves, holds, and onboarding timelines. It should also integrate with the platforms you actually use, including GunBroker, Authorize.net, NMI, POS systems, or a firearms-specific eCommerce stack.

A processor that cannot answer those questions clearly is usually not the right long-term fit for a gun shop.

How do you apply for an FFL merchant account online?

Applying online usually starts with a pre-underwriting review rather than a one-click instant signup. Most firearms-friendly providers will ask for your Federal Firearms License, business entity details, owner identification, EIN, bank information, processing history if you have one, projected monthly volume, average ticket size, refund policy, and your website or online sales channels. ATF’s licensing materials show that the FFL itself involves formal licensing and responsible-person disclosures, so underwriters naturally expect the merchant account application to match those legal records closely.

For online FFL sales, expect even closer reviews. The processor will want to understand what products you sell, whether you separate regulated firearms from accessories, how your checkout flow handles restricted items, and how you route firearm transfers to receiving FFLs instead of shipping directly to nonlicensees. That review is one reason specialized processors outperform generic sign-up tools for this category.

Can you get a merchant account for selling firearms online?

Yes. You absolutely can get a merchant account for online firearm sales, but not from every provider. The key is working with a processor and acquiring a relationship that knowingly accepts online FFL merchants. Providers like Payroc, Gearfire, Blue Payment Agency, SecureGlobalPay, EPIC Merchant Systems, and Signature Payments all market solutions for online or omnichannel firearm sellers. Their onboarding usually focuses on platform integration, lawful transfer workflows, fraud controls, and category transparency.

What does not work well is trying to process online firearm sales through providers that prohibit the category in policy. That approach may appear easier on day one, but it creates account-closure risk later.

What payment gateways work for online gun sales?

There is no single universal gateway for online firearms sellers, but a few names show up repeatedly in this space. Payroc explicitly references integrations with Authorize.net, GunBroker, NMI, PayTrace, and CyberSource, along with several gun dealer software stacks. Gearfire emphasizes its own integrated eCommerce ecosystem and AXIS POS pairing. Blue Payment Agency is commonly discussed in the context of Shopify-adjacent firearms-friendly gateway alternatives, while other high-risk providers use NMI or Authorize.net style gateway deployments depending on the merchant’s platform.

For most merchants, the right question is not just “which gateway is available?” but “which gateway is approved for my mix of products, platform, and shipping workflow?” That is where specialized underwriting matters.

What fees are typical for firearm merchant accounts?

Typical fees vary too much by volume, channel mix, chargeback history, and acquiring bank to quote a universal number honestly. Firearm merchants may face higher effective pricing than low-risk retail because the category can trigger more manual underwriting, monitoring, and reserve management. On top of the basic discount rate and transaction fee, merchants may see gateway fees, PCI fees, monthly account fees, chargeback fees, and, in some cases, rolling reserves or delayed funding terms. Providers like Payroc also market cash-discount and dual-pricing options that can shift more of the processing cost to the point of sale, but those models need to be evaluated carefully for legal, disclosure, and customer-experience fit.

So when merchants search for “compare FFL merchant account fees and rates,” the smart comparison is not just the rate sheet. Compare the total package: monthly minimums, gateway costs, hardware costs, reserve terms, funding time, cancellation terms, and whether the provider will still support your account six months later.

What underwriting red flags cause denials, holds, or reserves?

The most common red flags are not mysterious. They usually come down to incomplete or inconsistent documentation, undisclosed products or channels, a weak or non-compliant website, prior processing issues, large-ticket volatility, or uncertainty around online transfer compliance. Underwriters want the FFL, legal entity, owner ID, bank records, website, and stated business model to line up cleanly. They also want clarity on whether you sell regulated firearms, ammo, accessories, NFA items, range services, or event/gun-show volume. Specialized processors repeatedly emphasize that transparent, category-specific underwriting is what reduces surprise holds later.

For online merchants especially, vague product descriptions, missing policies, poor contact information, or checkout flows that do not clearly account for FFL transfer rules can slow approval or increase reserve risk. A clean, complete packet wins faster approvals.

What fraud, age-verification, and chargeback controls do processors expect?

At minimum, firearm merchants should expect to use AVS, CVV, and real-time fraud screening for card-not-present sales. The processor may also expect clear age and identity verification steps, documented FFL transfer procedures, order review rules for high-ticket transactions, and strong dispute documentation. FBI NICS requirements and ATF transaction-record expectations do not replace payment fraud controls, but they do shape how merchants build auditable workflows around each sale. ATF also revised Form 4473 in January 2026, which is another reminder that merchants should keep their compliance workflows current.

For chargebacks, the best defense is evidence. That means accurate receipts, signed acknowledgments where appropriate, delivery or transfer documentation, customer communications, and a checkout flow that does not create ambiguity about what was purchased and how it will be legally transferred.

What state laws affect firearms payment processing?

One important update for 2026 is merchant category code compliance. California’s AB 1587 requires payment card networks to make the firearms-and-ammunition MCC available and requires merchant acquirers to assign it beginning May 1, 2025. Colorado’s SB24-066 similarly requires assignment of the firearms MCC effective May 1, 2025. New York’s 2024 law, S8479/A9862, also requires the firearms MCC, and a 2025 amendment, S745/A439, narrows part of the language around ammunition dealers. Visa’s 2025 merchant data standards manual confirms that acquirers must assign ISO MCC 5723 to qualifying firearms retailers in California, Colorado, and New York where required by law.

That matters because merchants in those states should expect more precise coding and potentially more structured underwriting questions around product mix, transaction monitoring, and merchant classification.

How should gun stores compare high-risk merchant service providers?

The best way to compare providers is to look at four buckets.

First, compare category stability. Does the provider clearly support FFLs, or are you trying to squeeze into a platform that does not want the category?

Second, compare channel fit. A store doing 90 percent countertop sales needs something different from a GunBroker-heavy seller or a merchant running eCommerce plus range activity.

Third, compare integration fit. Payroc is strong on named integrations. Gearfire is strong for merchants already inside its ecosystem. Some processors are more consultative and custom, which can work well for merchants with unusual workflows.

Fourth, compare contract reality. Ask about reserve triggers, funding times, gateway fees, PCI costs, support responsiveness, and who the acquiring bank is. That is where the real differences show up.

Top-rated FFL merchant account providers in the US

For most merchants, the strongest shortlist today is:

TacticalPay

Payroc

SecureGlobalPay

Gearfire Payments

EPIC Merchant Systems

Signature Payments

That does not mean all six are identical. It means these are among the names that repeatedly show up because they explicitly speak to firearms merchants, not just generic “high-risk” businesses. The best choice depends on whether your priority is simple retail processing, gun-show mobility, GunBroker/eCommerce integration, ecosystem tie-ins, or more hands-on underwriting support.

FAQ

What are the best payment processors for firearm merchants?

TacticalPay, Payroc, SecureGlobalPay, Gearfire Payments, EPIC Merchant Systems, and Signature Payments are among the better-known firearms-friendly options.

Which companies offer merchant accounts for gun stores?

Specialized processors and high-risk providers do. Mainstream consumer-friendly platforms like PayPal and Square are poor fits because their policies restrict firearms-related sales.

How do I apply for an FFL merchant account online?

Expect to submit your FFL, business details, owner ID, EIN, bank information, website, and sales-channel information for manual underwriting.

Can I get a merchant account for selling firearms online?

Yes, but usually only through a processor that knowingly supports online FFL merchants and understands transfer compliance.

What fees are typical for firearm merchant accounts?

Pricing varies, but merchants should compare the full cost stack, including rates, gateway fees, PCI fees, chargeback fees, reserve terms, and funding speed.

What state laws should I know about?

California, Colorado, and New York all have firearms MCC requirements that affect how qualifying merchants are coded by acquirers.

The Right Processor Isn’t Just a Vendor, It’s Your Infrastructure

Choosing a payment processor for your firearms business isn’t a one-time decision. It’s a foundational part of your operation that impacts cash flow, compliance, customer experience, and long-term stability.

The best processors for FFL merchant accounts, including TacticalPay, Payroc, SecureGlobalPay, Gearfire Payments, EPIC Merchant Systems, and Signature Payments, all exist because this industry requires specialized underwriting and real compliance understanding.

But here’s what most merchants don’t realize:

Not all approvals are built to last.

At FFLMerchant, we don’t just help you get approved, we structure your account the right way from the start.

Through our direct experience working alongside Signature Payments and the North ecosystem, we’ve built access to multiple acquiring banks and firearm-friendly processing pathways. That means we’re not forcing your business into a single box, we’re matching you with the right setup based on how you actually operate.

That translates into:

- Stronger approval outcomes

- More stable processing relationships

- Fewer unexpected holds or shutdowns

- Better alignment for retail, eCommerce, GunBroker, and high-volume sales

We’ve worked in this space long enough to understand one thing clearly:

Firearm merchants don’t need generic solutions, they need the right structure from day one.

Apply with FFLMerchant and Get Approved the Right Way

If you’re ready to move forward with a firearm-friendly merchant account that’s built for long-term stability, not short-term approval:

Start with a pre-underwriting review before you submit.

We’ll help you:

- Identify potential red flags before they slow you down

- Structure your application for approval

- Match you with the right banking and processing setup

👉 Apply today with FFLMerchant and start processing with confidence.